Everything You Need to Know About Credit Scoring

By J.R. Robinson (April1, 2026)

In personal finance, investing tends to steal the spotlight, but understanding credit scoring is a critical and often overlooked financial skill that everyone should develop. Credit scores influence whether you can rent an apartment, buy a car, or qualify for a loan. They also determine the interest rates you will pay. The information used to calculate these scores is collected and maintained by the three major credit rneporting agencies: Equifax, Experian, and TransUnion. Their data feeds scoring models such as FICO and VantageScore, which translate your financial behavior into a three-digit number that ranges from 300-850.

My goal in writing this article was to squeeze all the most important information on building great credit into a single, easily digestible article. As you will read I explain how credit scores are calculated, address common misconceptions, and highlight key strategies for managing your credit wisely.

Understanding FICO and Vantage Scores

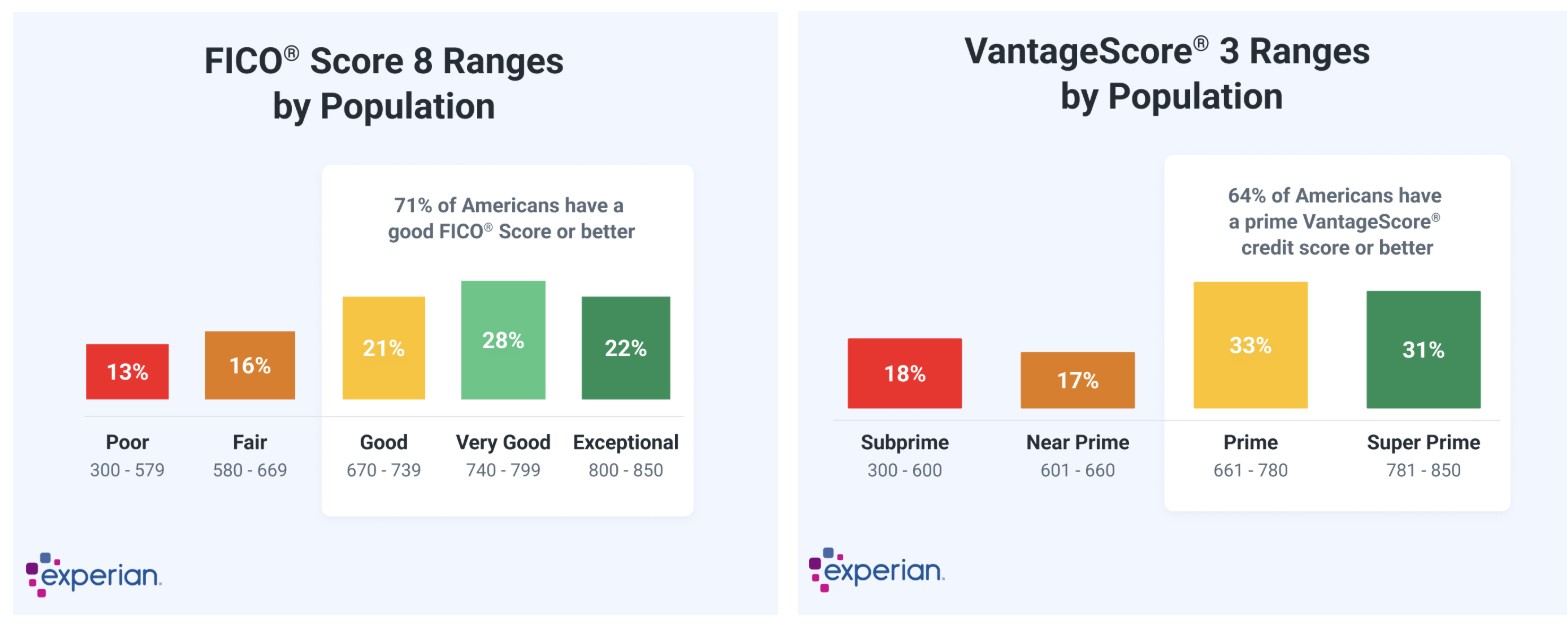

The charts below from Experian show the scoring ranges for FICO Score 8and Vantage 3.0 and how they score differently. Source: What is a Good Credit Score? (Experian)

How Credit Scores Are Calculated

Credit scores are derived from information in your credit report, which includes your borrowing and repayment history. While the exact formulas are proprietary, major credit bureaus consistently emphasize five core factors. Understanding these and their relative weightings in determining your score can go a long way to keeping your score healthy and high:

1. Payment History (35% weighting)

This is the most important factor. It reflects whether you pay your bills on time. Late or missed payments can significantly lower your score, while consistent on-time payments help build it. To drive home just how important this is, a single late payment (defined as more than 30 days past due) can drop your score by over 100 points and the negative impact can last seven years.

2. Credit Utilization (Amounts Owed) (30% weighting)

This refers to how much of your available credit you are using. For example, if you have a $1,000 limit and carry a $500 balance, your utilization is 50%. Lower utilization - generally below 30% - is viewed more favorably. Routinely maxing out credit cards is considered an indicator of financial distress.

3. Length of Credit History (15%)

The longer your credit accounts have been open, the better. A long history provides more data for lenders to evaluate your behavior.

4. Credit Mix (10%)

Having a variety of credit types. Credit cards are unsecured revolving credit. While home home equity lines are secured revolving credit. Mortgages, auto loans, and student loans are examples of installment credit. Having a mix of these can have a positive impact on your credit score as long as you always pay on time.

5. New Credit Activity (10%)

Opening several new accounts in a short period can signal risk and may lower your score temporarily.

Together, these five factors create a snapshot of your financial reliability.

The Truth About Multiple Credit Cards

Many young people assume that having multiple credit cards is harmful. In reality, when used responsibly, multiple cards can actually improve your credit score.

Having several cards increases your total available credit, which can lower your overall credit utilization ratio. For example, if you spread a $1,000 balance across cards with a combined $5,000 limit, your utilization is only 20%, which sends a positive signal to lenders.

However, there is a catch. Opening too many cards in a short period can trigger multiple hard inquiries and reduce your average account age, both of which may temporarily lower your score. Balance and timing are key.

Why You Shouldn’t Cancel Old Credit Cards

One of the most common mistakes young people make is closing old credit accounts. While it may seem logical to get rid of unused cards, doing so can hurt your credit score in two ways:

First, it reduces your total available credit, which can increase your utilization ratio. Second, it shortens your credit history, especially if the account you close is one of your oldest.

Credit bureaus emphasize the importance of maintaining long-standing accounts because they provide a stable record of responsible behavior. Keeping older cards open—even if you use them occasionally—can help strengthen your score over time. This bit of wisdom was part of my motivation for writing this article, because it runs counter to prevailing misguided wisdom that you should cancel an old card before getting a new one.

The Risk of Overusing a Favorite Card

Another common pitfall is relying too heavily on one credit card. Even if you pay your balance in full each month, maxing or nearly maxing out a single card can negatively impact your credit score.

This is because scoring models often evaluate utilization both overall and per account. High usage on one card - even if your overall utilization is low - can still signal risk. Spreading your spending across multiple cards can help avoid this issue and present a more balanced credit profile. This one can be tricky because you may be tempted to emphasize a favorite cash back, mileage or other rewards-based card for the majority of your purchases. One potential solution is to periodically request an increase in the spending limit on your favorite card. The increase may temporarily dip your score by a few points but the resulting lower credit utilization ration usually improves your score in the long run.

Hard vs. Soft Credit Inquiries

Credit inquiries are another important component of your credit profile, and understanding the difference between “hard” and “soft” inquiries is essential.

Soft Inquiries

Soft inquiries occur when you check your own credit or when a company performs a background or prequalification check. These do not affect your credit score.

Hard Inquiries

Hard inquiries happen when you apply for new credit, such as a loan or credit card. These inquiries are visible to lenders and can slightly lower your score, typically by a few points.)

While a single hard inquiry has minimal impact, multiple inquiries in a short period can raise concerns about financial risk and have a greater negative effect.

Common Credit Score Misconceptions

There are many myths about credit scoring that can lead to poor financial decisions. Here are a few of the most common:

Myth 1: Checking your credit score hurts it

This is false. Checking your own score is a soft inquiry and has no impact. All readers should also be aware that federal law requires the three agencies to provide your full credit history upon demand once per year. You may request your free report at AnnualCreditReport.com. A word of caution - there are many knock off websites with bad intentions. This is the only authorized website.

Myth 2: Carrying a balance improves your score

Noooooooo!!! You do not need to carry a balance to build credit. Paying your balance in full each month is actually the best strategy. ALWAYS. If you find yourself in a bind with credit you cannot quickly repay, search for lower interest rate alternatives such as a personal loan from a bank or even a loan from your 401(k). 0% balance transfer card offers may also buy you as long as 14-24 months to pay off the debt without paying interest. Most 0% offers hit you with a 3% up-front balance transfer fee, but that may still be far better than the 15%-25% annualized rates that many cards charge on carried balances.

Myth 3: Closing accounts improves your credit

As discussed earlier, closing accounts can reduce your credit history length and increase utilization, both of which can hurt your score. This is a common mistake and was part of my motivation for choosing to write on this topic. While it may be liberating to move past that first studend Discover card with a $1,000 spending limit that that your parents helped you set up when your were 18, you should cherish that card like an old friend.

Myth 4: All debt is bad

There are a few high profile self-anointed personal finance experts who preach this nonsense. Carrying high interest rate debt is never great planning. However, responsible use of credit—such as making on-time payments and maintaining low balances—can actually build your score and make it easier for you to qualify for attractive rates on a mortgage, HELOC, or auto loan.

The Rise of Alternative 900 Scoring Models

Traditional credit scores typically range from 300 to 850. However, newer scoring models - often referred to as “alternative” or expanded scoring systems- can extend up to 900.

These models, including newer versions of VantageScore, may incorporate additional data such as utility payments, rent, and streaming service bills. Programs like Experian Boost allow consumers to include such data in their credit profiles, potentially increasing their scores. A purpose of the models is to help lenders better evaluate the consumers with limited or thin credit histories. Simply put, on-time payments of r rent, utilities, and streaming services tend to be correlated with credit worthy consumers.

These modernized models are becoming increasingly more popular as lenders value the more detailed data points. If you see Vantage Score 4.0 or FICO 10T, you will know your lender is using them.

Parting Thoughts

Credit scoring may seem complex, but the underlying principles are straightforward. Pay your bills on time, keep your balances low, maintain older accounts, and apply for new credit cautiously. Understanding how factors like credit utilization, account age, and inquiries affect your score can help you make smarter financial decisions.

For young people, the key takeaway is this: credit is not just about borrowing money - it is about demonstrating reliability over time. By building good habits early, you can establish a strong credit profile that opens doors to future financial opportunities.

Another important point to remember is that the credit card issues have a vested interest in encouraging you to use your card often and to carry a balance. Their interests and yours are not aligned. While there is nothing wrong with applying for reward cards that align with your spending patterns and interests, the rules of responsible credit management described above should remain front-of-mind.

Ultimately, your credit score is a reflection of your financial behavior. With knowledge and discipline, it is a tool you can control - and use to your advantage. Save this article for future reference.

John H. Robinson is the founder of Financial Planning Hawaii and Fee-Only Planning Hawaii