YIELD SHOPPER By Financial Planning Hawaii JULY 2026

Yield Shopper is a service for helping Financial Planning Hawaii Clients keep abreast of current yields on money market funds, high yields savings accounts, CDs, treasuries, agency securities, municipal bonds, corporate bonds, and other popular fixed income investments.

JR’s Two Cents on the Fixed Income Marketspace - July 2026

HERE IS A SNAPSHOT OF FIXED INCOME RATES AS OF THE FIRST WEEK OF JULY 2026

Source: Charles Schwab fixed income trading desk.

*The Taxable Equivalent Municipal AAA Yield is calculated from the Municipal AAA Yield, and assumes a 35% federal tax rate. This does not reflect the effects of any state or local taxes, which, if applicable, may increase the taxable equivalent yield. For questions about calculating your individual rate, see your tax advisor. The following formula is used: Taxable Equivalent Municipal Yield = (Municipal AAA Yield) / (1.00 - 0.35).

In reviewing the yields in the table above, investors should keep in mind that the interest paid on treasury securities and certain government agencies (e.g. Federal Home Loan Bank, Federal Farm Credit Bank, and Tennessee Valley Authority) is exempt from state income tax. Interest from most (but not all) municipal bonds is exempt from federal income tax. Federally tax exempt municipal bonds issued within your residence state (or issued by U.S. territories such as Guam and Puerto Rico) are generally exempt from state income tax as well. Interest paid Certificates of Deposit, Corporate Bonds, and annuity contracts is subject to federal and state income tax. In comparing yields between these securities it may be necessary to calculate the tax-equivalent yield.

Taxable Equivalent Yield Calculator (Source: Fidelity)

Money Market Funds 7/12/2026

Fund Name & Symbol | 7-Day Yield | Link to Fact Sheet & Prospectus |

Schwab Prime Money Market Fund (SWVXX) | 3.46% | |

Schwab U.S. Treasury Money Fund (SNSXX) | 3.39% | |

Schwab U.S. Treasury Money Fund (Ultra Shares) SUTXX | 3.53% | |

Fidelity Prime Money Market Fund (SPRXX) | 3.35% | |

Fidelity Treasury Only Money Fund (FDLXX) | 3.32% | |

Vanguard Cash Reserves Fed MMF (VMRXX) | 3.56% | |

Vanguard Treasury Money Fund (VUSXX) | 3.64% |

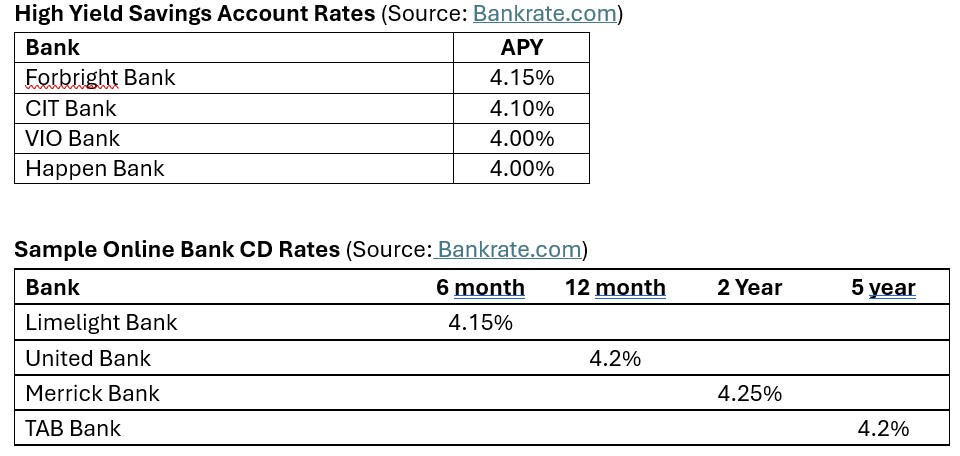

Readers will do well to compare the yields from these banks featured on Bankrate.com to the yields on CDs in the Schwab table above. There is a popular misconception that the yields on CDs are higher at online banks than on brokered CDs available through Schwab, Fidelity, and Vanguard. While there are occasionally individual banks that may offer a special rate that is nominally higher, for the most part, brokered CD rates are extremely competitive when compared to the online bank market space.

Always remember: Friends Don't Let Friends Buy Bond Funds (or ETFs)

Readers of my commentary know I do not ever recommend bond mutual funds or ETFs. The primary reason for this position is I believe the risk-free portion of client portfolios should truly be risk-free. Individual bonds and CDs are generally regarded as risk-free if held to maturity. Bond mutual funds and ETFs cannot provide such assurances. In a rising interest rate environment, investors are often unpleasntly suprised by the decline in value of the so-called "conservative" bond funds in their reitrement accounts.

I have written many articles on this topic. This position is echoed by retirement researcher and financial planning industry thought leader Wade Pfau, PhD, CFA. Links to Wade’s commentary on this topic are as follows:

3 Ways to Incorporate Bonds Into Your Retirement Strategy (Retirement Researcher)

Why Bond Funds Don’t Belong in Retirement Portfolios (Wade Pfau, Advisor Perspectives)

Laddering with Individual Bonds (Retirement Researcher)

John H. Robinson is the founder of Financial Planning Hawaii and Fee-Only Planning Hawaii and a co-founder of retirement simulation software, Nest Egg Guru.