JR'S Two Cents - February 2026

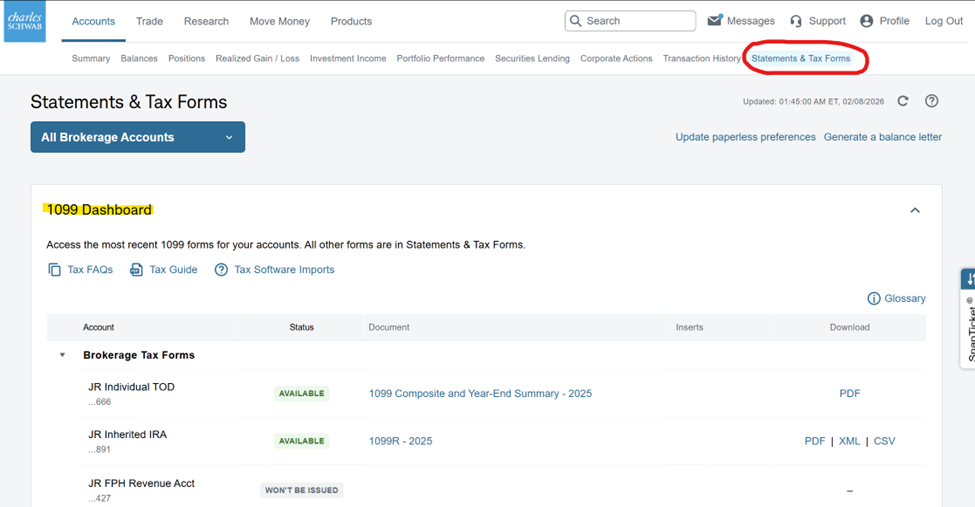

Looking for your Schwab Tax Documents?... You don’t need to wait for the mail - just log into the Schwab Alliance website and check your documents’ status on the Schwab 1099 Dashboard.

For clients who took taxable distributions from retirement accounts, including inherited IRAs, in 2025, the 1099-Rs have been issued and are posted on the Schwab Alliance website. Composite 1099s (1099-INT, 1099-Div & 1099-B) are being rolled out through out February.

NOTE: Clients who transferred from NFS to Schwab in advance of our migration to Charles Schwab, may receive 1099s from both custodians.

My Two Cents on Hawaii’s Proposed “Wealth Tax… Hawaii Senate Bill 313establishes a wealth tax of 1% of the state net worth of each individual taxpayer who holds $20,000,000 or more in the state. If passed, bill would go into effect on January 1, 2030. The tax would be paid every three years. A journalist from Financial Planning magazine asked me to opine on the idea. Here is a link to the article and the excerpt with my comments.

As ultrarich sweat, advisors tackle 'ripple effects' of proposed billionaire tax (Financial Planning, February 6, 2025)

"While Hawaii's wealth tax proposal is still under consideration, it's unlikely to pass, according to John Robinson, the founder of Financial Planning Hawaii in Honolulu.

"My guess is that this law will face stiff opposition, since the hardest hit people would be Hawaii residents who own property and businesses in the state and who report their securities portfolio realized gains, interest and dividends on their Hawaii returns," Robinson said. "While increasing sales and travel-related tax on foreign and mainland tourists and raising property tax on owners from overseas or the U.S. mainland are easy populist targets, placing the highest burden on our own state's business owners, farmers and landowners will not sit well. My guess is that this bill has no shot at becoming law."

Why AI Chat Bots Can’t Be Trusted for Financial Advice

AI portends to disrupt virtually every industry, one of the earliest and theoretically easiest targets is the business of financial advice. It is common in daily client communications for clients to ask me about a piece of advice they gleaned from ChatGPT. Like everyone else with an Internet connection, I am increasingly relying on AI for search too. I bounce around between Perplexity, Gemini, and Chat GPT, and, as a domain authority in the personal finance and portfolio management space, I can tell you that the AI is decidedly not a reliable source of financial planning guidance – or tax and legal guidance for that matter.

This surprising deficiency is the feature story in today’s Wall Street Journal - Why AI Chatbots Can’t Be Trusted for Financial Advice: They’re Sociopaths (WSJ, 2/18/26). The article suggests that part of the problem is that the LLMs are not trained to understand concepts of behavioral economics such as principles of loss aversion. In my experience, it seems to me that the AI models are giving too much weight to low domain authority sources.

However, another likely source of the misinformation problem is that the LLMs most of us are using are the free versions, which are probably 6-12 months old and, thus, hopelessly antiquated by AI growth standards. To be clear, I am not dismissive of the future of AI or of the encroachment threat it poses to my livelihood. To the contrary, to survive and thrive financial planners need to adapt to AI, incorporate it to improve productivity and client experiences, and articulate the ways we add value to consumers lives that cannot be delivered by AI. Expect this to be a recurring theme in Financial Planning Hawaii content and communications.

A Cult of Personality?... Cathie Wood is a former Capital Group portfolio manager who rose to fame when her flagship Ark Innovation ETF returned 153% in 2020. Since then, her fund returns have been (ahem) “uneven.” According to TheStreet.com, Ark Innovation has generated a five-year annualized return of -13.83% versus a positive 13.92% annualized rate for the S&P 500 Index through February 6, 2026. Yet such wealth-crushing returns do nothing to dim her media star, as illustrated by her latest headline making trade - Cathie Wood buys $43 million of megacap tech stock

Related Reading: A superstar investor with the Midas touch or just lucky? The puzzle of Cathie Wood (NPR, May 22, 2022)

Don’t Forget to Take Your RMDs!

At the end of last year, Vanguard published an article revealing that approximately 7% of its clients who have RMDs, failed to take them. The author of the article estimated exptrapolated its data across the entire U.S. population and estimated that the IRS penalties due will be between $680 milliion and $1.7 billion.

Each year, Financial Planning Hawaii encourages clients who are over age 73 or who have inherited IRAs to take their RMDs earlier in the year so as not to forget at year-end. Alicia and Sue have already begun reaching out.

NOTE: IRA holders may consolidate the RMD from multiple IRA accounts. However, consumers age 73+ who have 401(k) and/or 403(b) accounts from former employers, must take RMDs from each plan account.

Financial Planning Hawaii has the RMD amounts for all clients, but if you wish to check our math or have held away retirement accounts that are beyond our scope, here are hand links you can use to run your own numbers.

CHARLES SCHWAB CALCULATE YOUR RMD

CHARLES SCHWAB INHERITED IRA RMD CALCULATOR

John H. Robinson is the founder of Financial Planning Hawaii and Fee-Only Planning Hawaii and a co-founder of retirement simulation software-maker, Nest Egg Guru.

Although representatives of Financial Planning Hawaii may review client tax and legal documents, deliver tax-reporting documents, and raise awareness of potential tax and/or estate planning related mistakes or opportunities, none of this information should be construed as constituting specific tax or legal advice. All clients are encouraged to consult with their respective CPAs and/or attorneys for such guidance.