YIELD SHOPPER - JUNE 2026

YIELD SHOPPER By Financial Planning Hawaii

Your Go-To Source for Interest Rates on CDs, Bonds, and other fixed income investments

The purpose of Yield Shopper is to keep Financial Planning Hawaii clients apprised of the general level of interest rates on various fixed income investments, including money market mutual funds, bank money market and savings accounts, certificates of deposit (CDs), treasury and agency securities, municipal and corporate bonds, and short-duration bond ETFs. Readers should know that all yields are subject to change without notice. The yield data presented is for informational purposes only.

JR’s Two Cents on the Fixed Income Marketspace (June 3, 2026)

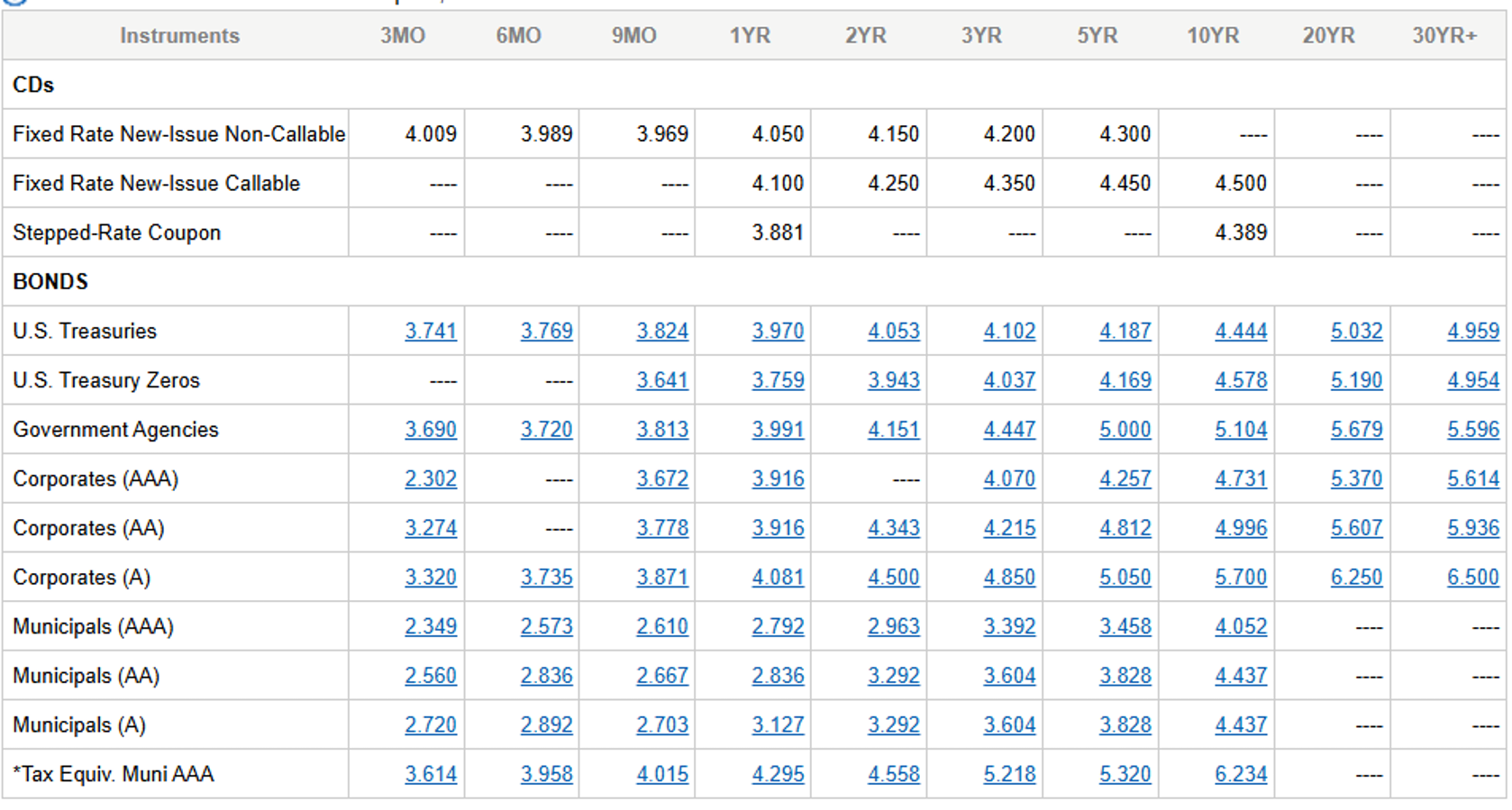

At this time, we are holding more than $100 million of client assets in Schwab money market funds. The most common question I field these days is, “Isn’t there something paying more?” Rest assured the outsized allocation to money market funds is not due to slothfulness or neglect. The reason for stockpiling all this cash is not for roughly 3.5% money market fund yields, but rather because the money market funds offer a risk-free, liquid placeholder while we wait for interest rates to rise again. And early indications are that rates may be beginning to rise already. As you can see, the yields on CDs have ticked up to 4% again.

I believe they will continue to creep higher, however, for clients who are beginning to salivate over the 4%+ yields on CDs, I have no problem at all locking in those rates for 12-18 months. Just reach out to Sue or me and we can make that happen.

In the meantime, here are some takeaways from the data below:

- I get the sense that people always wonder if the brokered CD market is competitive with the direct-to-consumer offered CDs you see on NerdWallet or Bankrate.com. Compare the Fixed Rate New-Issue Non-Callable CDs in the Schwab Table to the Bankrate.com yields below. You are not missing out on yield if you purchase a brokered CD. They are competitive with the highest rates in the country.

- Callable Government Agency Bonds may be worth a look. You may be able to get 4.5%-5% in the 2-5 year range. However, I advise making sure the Agency bond you purchase has at least 6 months of call protection.

In Comparing the Cash-like ETFs, the Schwab Short Term (1-3 year) treasury ETF (SCHO) with its 4% distribution rate, looks compelling next to its peers. It reflects the recent rise in 1-3 year treasuries relative to the 3-12 month treasuries

- Source: Charles Schwab fixed income trading desk.

- *The Taxable Equivalent Municipal AAA Yield is calculated from the Municipal AAA Yield, and assumes a 35% federal tax rate. This does not reflect the effects of any state or local taxes, which, if applicable, may increase the taxable equivalent yield. For questions about calculating your individual rate, see your tax advisor. The following formula is used: Taxable Equivalent Municipal Yield = (Municipal AAA Yield) / (1.00 - 0.35).

In reviewing the yields in the table above, investors should keep in mind that the interest paid on treasury securities and certain government agencies (e.g. Federal Home Loan Bank , Federal Farm Credit Bank, and Tennessee Valley Authority) is exempt from state income tax. Interest from most (but not all) municipal bonds is exempt from federal income tax. Federally tax exempt municipal bonds issued within your residence state (or issued by U.S. territories such as Guam and Puerto Rico) are generally exempt from state income tax as well. Interest paid Certificates of Deposit, Corporate Bonds, and annuity contracts is subject to federal and state income tax. In comparing yields between these securities it may be necessary to calculate the tax-equivalent yield.

Taxable Equivalent Yield Calculator (Source: Fidelity)

Money Market Funds

Fund Name & Symbol | 7-Day Yield | Link to Fact Sheet & Prospectus |

Schwab Prime Money Market Fund (SWVXX) | 348% | |

Schwab U.S. Treasury Money Fund (SNSXX) | 3.41% | |

Schwab U.S. Treasury Money Fund (Ultra Shares) SUTXX | 3.50% | |

Fidelity Prime Money Market Fund (SPRXX) | 3.26% | |

Fidelity Treasury Only Money Fund (FDLXX) | 3.51% | |

Vanguard Cash Reserves Fed MMF (VMRXX) | 3.58% | |

Vanguard Treasury Money Fund (VUSXX) | 3.60% |

Cash & Cash-Like ETFs

Issuer | APY | Link to Fact Sheet & Prospectus |

Vanguard 0-3 Month T-Bill ETF (VBIL) | 3.56% | |

iShares 0-3 Month Treasury ETF (SGOV) | 3.54% | |

SPDR 1-3 Month T-Bill ETF (BIL) | 3.69% | |

Schwab Short Term U.S. Treas ETF (SCHO) | 4.0% |

High Yield Savings Account Rates (Source: Bankrate.com)

Bank | APY |

CIT Bank | 4.10% |

Vio Bank | 4..03% |

Bread Savings | 4.00% |

Lending Club | 4.00% |

Sample Online Bank CD Rates (Source: Bankrate.com)

Bank | 9 month | 12 month | 2 Year | 5 year |

Forbright BAnk | 4.15% |

|

|

|

Popular Bank |

| 4.11% |

|

|

Merrick Bank |

|

| 4.2% |

|

Merrick Bank |

|

|

| 4.2% |

- Readers of my commentary know that I do not ever recommend bond mutual funds or ETFs (aside from money market ETFs). I have written many articles on this topic, which are included below. This position is also shared by retirement researcher and financial planning industry thought leader Wade Pfau, PhD, CFA. Links to Wade’s commentary on this topic are as follows:

- 3 Ways to Incorporate Bonds Into Your Retirement Strategy (Retirement Researcher)

- Why Bond Funds Don’t Belong in Retirement Portfolios (Wade Pfau, Advisor Perspectives)

- Laddering with Individual Bonds (Retirement Researcher)

- JOHN ROBINSON’S RECENT COMMENTARY ON FIXED INCOME INVESTMENTS FROM THE FPH BLOG

- Short-Term Laddered Bond ETFs vs. Short Term Bond Funds (9/25/2025)

- Cash ETFs: The New “New Thing” in the Search for Yield and Safety? (9/25/2025)

- Government Money Market Funds Are Not All The Same (2/9/2025)

- Why I Always Say “Friends Don’t Let Friends Buy Bond Funds (4/1/2025)

- Not So Hot TIPS (11/1/2024)

- Keeping Score – A Running Record of My Interest Rate and Fixed Income Guidance Since 2020 (6/5/2024)

- Where to Fish for the Best Fixed Income Yields Today (3/4/2024)

- Interest Rates on CDs Plummeted in November. How to Invest Now (12/3/2023)

- How to Invest When the Yield Curve is Inverted (9/8/2023)

- It's Time to Start Laddering Certificates of Deposit Again (5/21/2023)

- Is Your Cash Working as Hard as it Should Be? 2/16/2023

- How to Invest in Bonds and CDs Now that Interest Rates Have Risen 12/10/2022

- Where to Stash Cash Now 9/29/2022

- I was Right About Interest Rates 9/29/2022

- The Time to Buy Series I Savings Bonds is NOW! 4/18/2022

- Why Friends Don’t Let Friends Buy Bond Funds (3/1/2022)

- Saying that the Bull Market in Bonds is Over is NOT Market Timing 12/10/2021

- Negative Returns Ain’t Much of a Living (8/9/2021)

- Looking for Yield in All the Wrong Places (5/25/2021)

- John H. Robinson is the founder of Financial Planning Hawaii and Fee-Only Planning Hawaii and a co-founder of retirement simulation software, Nest Egg Guru.

- Financial Planning Hawaii is an SEC-Registered Investment Adviser (RIA). Registration as an investment adviser does not imply any level of skill or training. For verification of Financial Planning Hawaii's regulatory status, all website visitors are encouraged to visit the SEC Investor Advisor Public Disclosure website. The site allows you to search by firm name and by adviser name. It provides detailed information about the firm's business model and each investment adviser representative's professional experience, educational background, and disclosure history.

- Financial Planning Hawaii's 2026 SEC Form ADV | Financial Planning Hawaii's 2026 Customer Relationship Summary